The Role of Bond Funds in Your Portfolio

Posted by Richard on June 9, 2015

Bonds are popular investment vehicles because they pay interest income with a promise to pay back the initial investment after an agreed-upon period of time. Bond mutual funds may be even more popular among those seeking an income component in their portfolio because they offer a lower-cost, professionally managed, diversified alternative to individual bonds. However, before determining whether bond funds will help meet your income needs, compare the goals, similarities, differences, and risks of bonds and bond funds.

What Is a Bond?

A bond is an “IOU” for money loaned by an investor to the bond’s issuer. In return for the use of that money, the issuer agrees to pay interest to the investor at a stated rate, known as the “coupon rate.” When the loan is paid back at the end of that time period — when the bond “matures” — the issuer repays the investor’s principal.

Because bond prices generally do not move in tandem with stock investments, they may help provide balance in an investor’s portfolio. They also provide investors with a steady income stream. Zero coupon bonds are the only exception, in that they provide no cash flow but are sold at a deep discount to their face value; the investor then receives the full face value of the bond at maturity.

Bonds come in a variety of forms, each bringing different benefits, risks, and tax considerations to an investor’s portfolio. Most bonds fall into four general categories: corporate, government, government agency, and municipal. Corporate bonds are issued by corporations and can be among the riskiest of all bonds. On the other hand, government bonds are among the safest because they are issued by the U.S. Treasury and backed by the full faith and credit of the U.S. government. The risks associated with government agency and municipal bonds vary, but usually fall in between corporate and government bonds on the risk spectrum.

Bond Mutual Funds

Combining many different bonds in one portfolio in order to pursue a stated objective, a bond mutual fund can provide a diversified fixed-income element to an investor’s portfolio. Because they aim to provide a steady stream of income, bond funds are suited to investors seeking to balance the fluctuations of stock investments while striving for protection of principal and current income. Bond funds may be most appropriate for investors nearing retirement and others who do not tolerate well large fluctuations in the value of their investments. Before investing in bond funds, however, investors should consider the risks of individual bonds and how they might affect a fund.

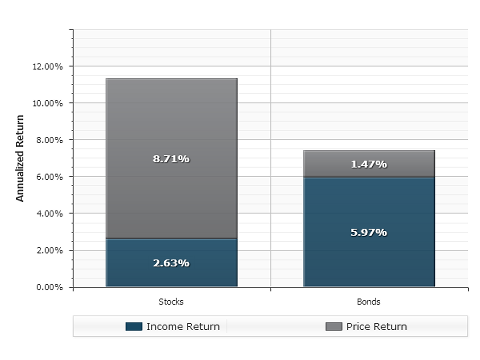

Components of Total Return, 1985-2014

While stocks have historically provided income and capital appreciation, the total return of bonds has been composed primarily of interest income. Source: ChartSource®, Wealth Management Systems Inc. Based on the 30-year period ended December 31, 2014. Stocks are represented by Standard & Poor’s Composite Index of 500 Stocks, an unmanaged index generally considered representative of the U.S. stock market. Bonds are represeted by the Barclays U.S. Aggregate Bond index, an unmanaged index generally considered representative of the broad, U.S., investment-grade fixed-income market. It is not possible to invest directly in an index. Past performance is no guarantee of future results. Copyright© 2015, Wealth Management Systems, Inc. All rights reserved. Not responsible for any errors of omissions. (CS000037)

Risks

Some bonds hold “credit risk,” or the risk that the bond issuer will go into default before the bond reaches maturity. In that case, you may lose some or all of the principal amount invested and any outstanding income that is due. Bonds are often rated by Moody’s and Standard & Poor’s (S&P). Ratings run from Aaa (Moody’s) or AAA (S&P) through D based on the issuer’s creditworthiness; Aaa and AAA are the highest credit ratings. Bond funds also can be issued ratings based upon the credit quality of their underlying bonds.

Like stocks, bonds can present the risk of price fluctuation (or “market risk”) to an investor who is unable to hold them until their maturity date. If an investor is forced to sell — or liquidate — his bond before it matures, and the bond’s price has fallen, he will lose part of his principal investment as well as the future income stream. Another risk common to all bonds is interest rate risk. When interest rates in the economy rise, a bond’s price will usually drop, and vice versa.

Individual bond investors need not worry too much about interest rate and market risk if they intend to hold their bonds until maturity. However, bond mutual fund investors should consider these forms of risk because fund managers can buy and sell bonds as often as they deem appropriate to meet the fund’s objective. Fund investors therefore risk loss because of fluctuations in the value of the fund.

Types of Bond Funds

Bond funds also come in a variety of forms, each striving to serve a different purpose based on the underlying individual securities. And like individual bonds, different bond funds hold different risks and sometimes offer tax benefits. Some of the more popular types of bond funds include U.S. government, corporate, and municipal bond funds.

Because U.S. government funds are composed of securities backed by the full faith and credit of the U.S. government, they hold little credit risk. They can, however, be affected by changes in interest rates and market conditions, and risk not keeping pace with inflation. U.S. government funds are taxed at the federal level, but are exempt from state tax. These funds generally appeal to investors seeking steady income and solid protection of principal.

Depending on their objective, corporate bond funds may invest in a variety of corporate issues with different, and perhaps even substantial, credit risks. In addition, they can be subject to interest rate and market risk. But remember that more potential risk usually means higher potential yields; therefore, these funds may suit investors who can withstand a bit of risk in pursuit of higher income.

Municipal bond funds generally invest in the higher-quality, federal tax-free issues of state governments and municipalities. Because of their potential benefits when compared to taxable securities, municipal bond funds can be appropriate for investors in the higher tax brackets. These are also subject to interest rate and market risk.

| Strategies to Help Reduce Risk When Investing in Bonds |

|

Choose the Fund That Meets Your Need

Although every bond fund comes with its own risk, you should balance the risks with the overall benefits of fund investing: Diversification can help lower overall risk in the fund1; professional management can save you the hassle of having to research and evaluate the thousands of individual bonds on the market; and lower initial investment requirements help ease accessibility to a wide variety of bonds. The best strategy is to work with your investment advisor to determine your fixed-income needs, identify a fund that will help meet those needs, and evaluate the risks associated with it.

Points to Remember

- Bonds provide an income stream and help diversify a stock portfolio.

- A bond’s total return includes both income and capital appreciation or loss. Bond prices fluctuate with changes in interest rates.

- Bonds are also subject to credit risk.

- Investors can buy individual bonds and bond mutual funds. Holding bonds to maturity eliminates market risk; bond funds will fluctuate in value.

- Investing in bond mutual funds allows individuals to diversify among many different bond issues, thereby reducing credit risk. Interest rate risk can be reduced by investing in shorter-term bonds, or by using a ladder or barbell strategy.

Source/Disclaimer:

1Diversification does not ensure against loss.

Required Attribution Because of the possibility of human or mechanical error by Wealth Management Systems Inc. or its sources, neither Wealth Management Systems Inc. nor its sources guarantees the accuracy, adequacy, completeness or availability of any information and is not responsible for any errors or omissions or for the results obtained from the use of such information. In no event shall Wealth Management Systems Inc. be liable for any indirect, special or consequential damages in connection with subscriber’s or others’ use of the content.

© 2015 Wealth Management Systems Inc. All rights reserved.